Market Outlook

Market Outlook

| April 2026 |

|

|

Amongst developed European economies, German index DAX was up by 7.1% followed by French CAC 40 Index (+3.8%) and FTSE 100 Index (UK) by 2%. US index Nasdaq was up by 15.3%, while S&P 500 was up by 10.4%

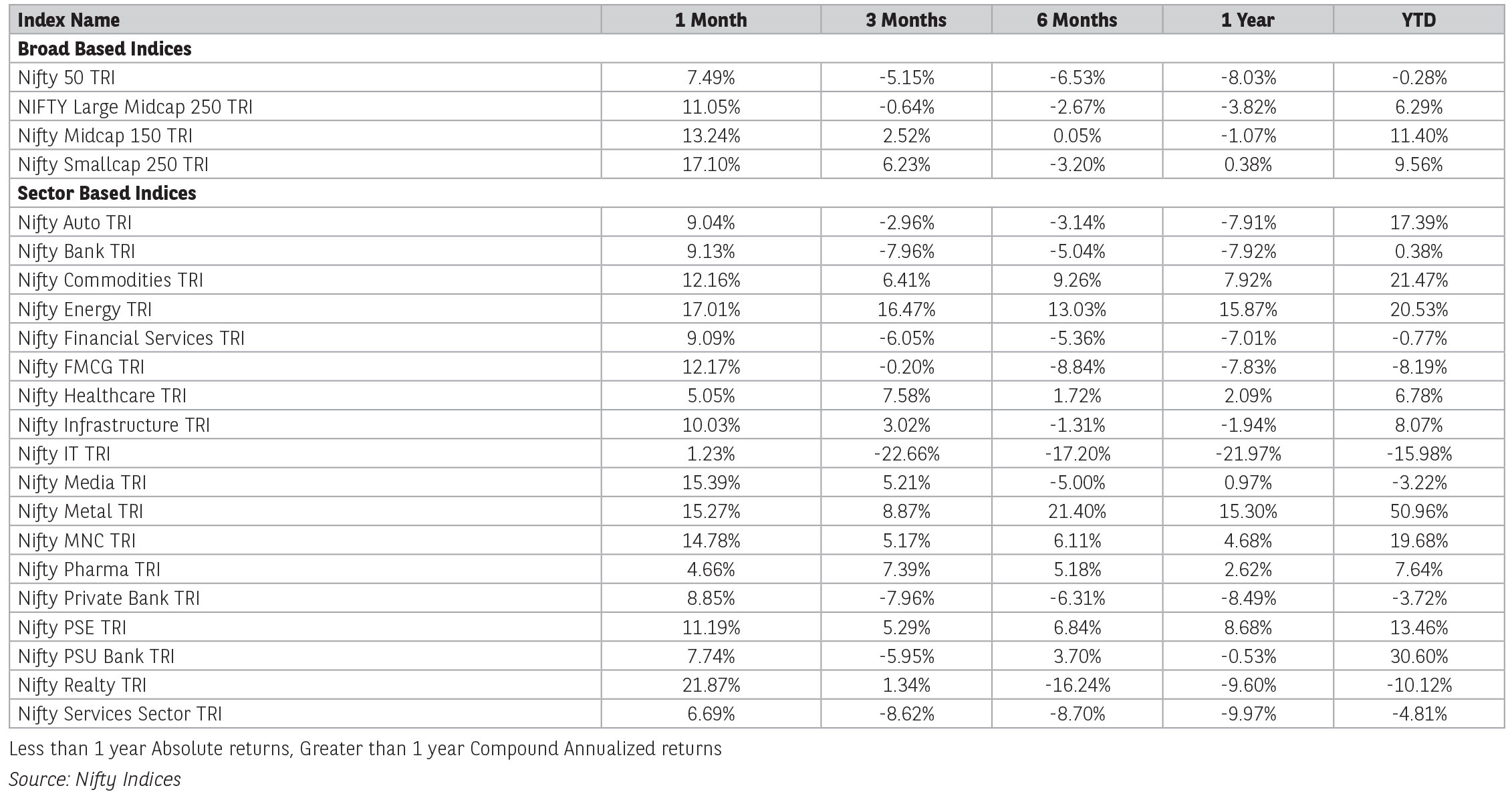

Indian midcap and small cap index saw sharp rally during the month with Nifty Small Cap 250 Index up by 17% and Nifty Midcap 150 Index by 13.2%. Sector wise all the sectors were in green with BSE Realty by 21.4%, followed by BSE Cap Goods (+20.2%), BSE Metals (+14.6%), BSE Consumer Durables (+12.3%), Consumer Discretionary (+12%), BSE Banks (+9.1%), BSE Oil (+8.3%) and BSE Healthcare (+6.8%).

With geo-political risk, global macro headwinds, weakening rupee and risk of inflation inching up due to rising crude oil prices, FPI flows in April 2026 remained negative with net outflow of USD 4.2bn. Amongst emerging economies, Brazil continues to see positive inflows for CY2026 with net inflow of USD 1.6bn in April. After a massive sell off, Taiwan and South Korea saw net inflow of USD 8.4bn and USD 599mn respectively led by strong demand in Artificial Intelligence (AI) and Semi-conductor segment.

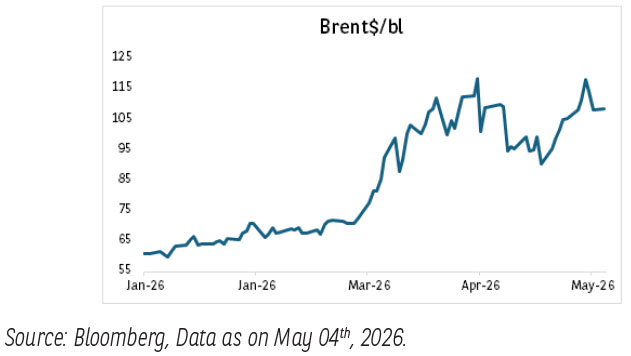

On 8th April 2026, US-Iran announced a two-week ceasefire for negotiations. However, after a failed attempt, US extended the ceasefire till 21st April 2026. The Strait of Hormuz continues to remain closed, disrupting global supply chain and energy markets. On account of the current crude crisis and higher energy prices the IMF has cut its global growth forecast by 20 bps. Growth is expected to be at 3.1% in 2026 and 3.2% in 2027.

Locally, RBI has kept the repo rate unchanged at 5.25% and stance of policy also remains unchanged at neutral. RBI remains focused on growth and there was no indication of a rate hike anytime soon. Manufacturing activities slowed down in March due to cost pressure, market uncertainty, and Middle East crisis leading to softer increases in new orders and output. Manufacturing PMI eased to 53.9 in March 2026 as against 56.9 in February, lowest since June 2022. Services PMI declined to 57.5 in March 2026 from 58.1 in February 2026. Exports declined 7.4% YoY in March 2026 to USD 38.9bn while imports declined 6.5% YoY to 59.6bn primarily due to decline in oil imports.

Corporate India started reporting its quarterly numbers. 161 companies out of Nifty 500 companies reported double digit growth for Q4FY26. Sales/EBITDA/PAT grew by 12.8%/11.6%/14.2% respectively. For the banking sector, system saw a bump in credit growth coming at 17% YoY with growth being broad-based across sectors. Key management commentaries suggest pickup in personal loans, continued growth momentum in gold, business banking and mid-corporates segments. The quarter witnessed meaningful reduction in slippages and better recoveries leading to improvement in credit cost. IT services companies reported revenue growth lower than expectations due to client specific issues and delay in the deal ramp ups. Slight margin contraction was also seen this quarter led by seasonality and select wage hikes which was offset by currency gains.

The impact of elevated oil prices and depreciation of rupee is yet to impact corporate India’s profitability. Resolution of the West Asia conflict, progress of monsoon, potential supply chain disruptions and input cost pressures, will be key monitorable. These can weigh on inflation and growth dynamics, especially in H1FY27. On the positive side, the current result season remains upbeat so far, water reservoir levels appear to be adequate, companies have not yet raised material red flags on demand due to the war, there are hints of private capex picking up (via both organic and inorganic route), all of which will likely keep demand driven nominal growth healthy in the year. Trailing Nifty valuations have now reverted to lower than the historical average to a PE of 22.3x as of April-end, as compared to the 10-year average trailing Nifty PE of 23.2x.

Source: Kotak Securities/Capital 360 ONE, Industry reports. Data as on April 30, 2026.

Global Economy –

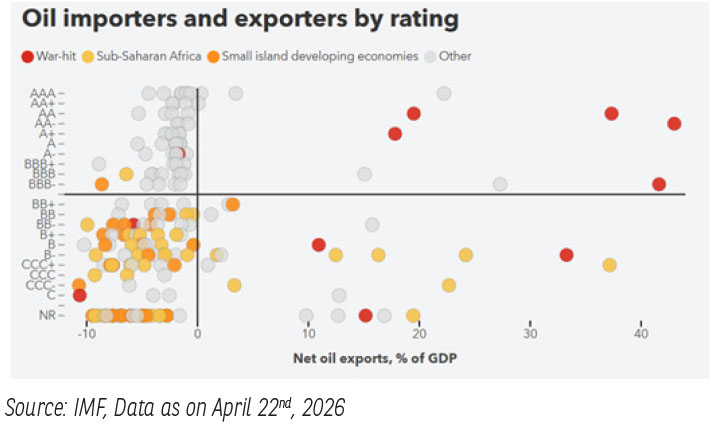

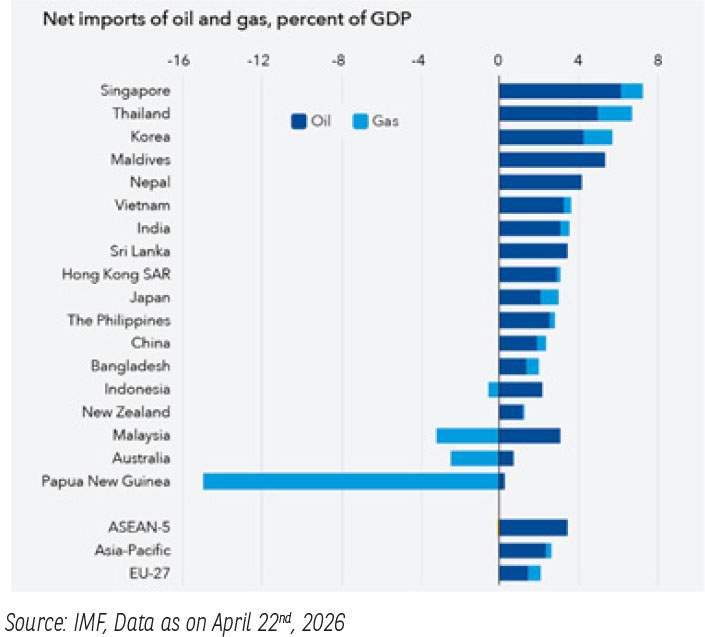

The ongoing conflict in West Asia has reignited global inflationary concerns, primarily driven by its impact on energy markets. What initially appeared to be a short-term spike in crude oil prices is now showing signs of persistence, as supply disruptions continue to deepen. With transit channels under strain, the sustained elevation in oil prices is increasing cost pressures across economies, thereby amplifying fears of prolonged inflation on a global scale. The exposure to higher oil prices and supply uncertainty differ across countries shaped by whether they import or export, and how much policy space they have to respond.

In the cusp of the war, Asian economies are facing the brunt, being the major buyer of oil and gas shipped through the Strait of Hormuz. Asian economies account for about 80% of LNG exported through the waterway. This disruption is already causing local shortages of petroleum products and gas, especially in countries with limited stockpiles. The direct impact is visible in their currencies of net importers of crude and gas, facing depreciating pressures. The second related impact is spillovers on import inflation and subsequently on rates.

Interest rates in advanced economies are generally expected to remain on hold reversing any outlook on softening of rates as to maintain disinflation. In US Fed made no policy move in line with expectations. The federal funds stayed at 3.5%- 3.75%. Although the voting pattern reflected, FOMC was moving closer to being explicitly neutral with three dissents in favour of shifting to a neutral bias. Powell continued with its ties with FED as a noninterfering governor in way to fight for FED’s independence. He will remain on the Fed board, acting as a central bank governor. The upcoming FED chair Kevin Warsh, fuels uncertainty about the hawkishness of FED’s future policy outlook.

In Japan, where inflation expectations are rising to near target, the central bank is expected to remain on pause while withdrawing accommodation during the first round of the energy shock. EU too is facing inflationary pressures driven by high gas prices. Less fiscal space since the pandemic and rising interest burdens, and now higher energy prices are raising fiscal concerns.

One part of the West Asia crisis was hitting supply but higher prices has also led to demand destruction affecting global growth. Most notably, petrochemical producers have curtailed operating rates as feedstock supply dried up, Households and businesses using LPG have also been impacted, while flight cancellations across the Middle East, parts of Asia and Europe have led to a sharp drop in jet fuel consumption. A growing number of countries have implemented policies to reduce demand, while others have put in place measures to shield consumers from the full impact of rising fuel prices. Overall, global oil demand is estimated to contract by 800 kb/d year-on-year in March and by 2.3 mb/d in April-2026. This stems out from a direct impact of reducing economic activity amidst restricted supply and elevated prices. Resuming flows through the Strait of Hormuz remains the single most important variable in easing the pressure on energy supplies, prices and the global economy.

Domestic Economy-

Domestic high-frequency indicators for March, in general, do not reflect much adverse impact of the global supply chain bottlenecks as some of the key risks have been contained by the Government, ensuring uninterrupted availability of petroleum products across the country. Overall demand conditions remained resilient with greater support from rural areas.

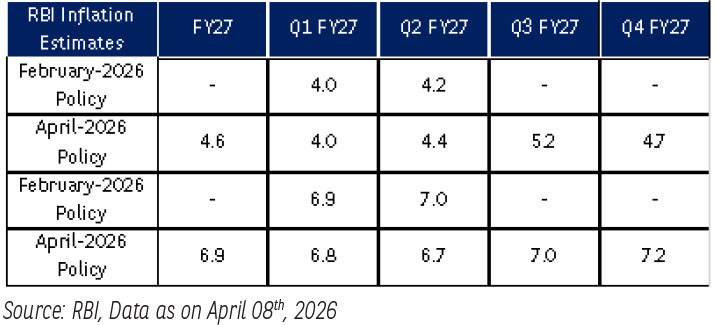

Trade deficit narrowed in March falling to a nine-month low. On a sequential basis, exports expanded, while imports contracted in March 2026. The conflict in West Asia led to a decline in exports and imports from the region. Amidst the geopolitical chaos, RBI in April-2026 monetary policy meeting decided to continue with a pause on repo rate and retained the neutral stance. The key reading in the policy was around MPC’s inflation and growth projections which reflect the recent shocks from elevated brent prices and spillovers from the West Asia war. Inflation is projected at 4.6% y/y for FY27. The future trajectory of inflation will mainly be guided by evolving geopolitical situation and the upcoming monsoon season. RBI’s language on domestic growth was concerned with recent impact on economic activity. Therefore, RBI has projected domestic growth at 6.9% for FY27 vs 7.6% in FY26. Importantly RBI continued to give comfort on the liquidity conditions in the economy and reiterated its proactive approach on liquidity management.

Domestic Inflation-

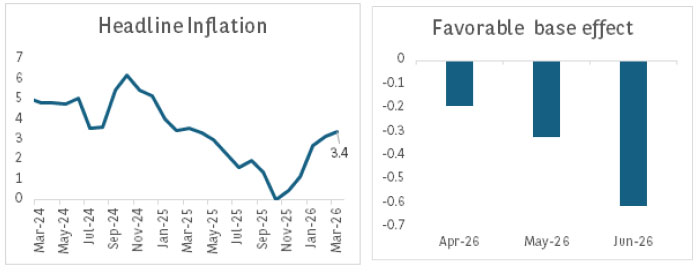

- The trajectory of inflation has seen an intercept shift in March-2026. Seasonal uptick in food prices plus spillovers of elevated fuel prices due to ongoing west Asia conflict led to higher momentum in domestic inflation.

- March CPI rose marginally to 3.4% y/y vs 3.2% y/y in Feb-26 as food, fuel prices inched up. Core inflation was at 3.7% y/y in Mar-2026, vs 3.4% y/y in Feb-2026.

- On a sequential basis, headline CPI inched up by 0.26% m/m led by broad base increase in the basket prices.

- Core inflation increased by 3.7% y/y in March 2026. Overall, the prices were generally stable in the core basket.

- Transfer of few items like higher airfare, gold prices etc. are partially remaining. Also, the estimate suggests that the pass through of higher input costs by companies to consumers is yet to begin.

- Remaining transfer of airfares prices, input cost inflation, LPG price hikes, higher food inflation in summer month etc. will keep the headline inflation higher than the current sub 3.5% inflation trend to a sub 4% headline number.

- CPI in Q1 and Q2 FY27 is expected to remain above RBI’s target of 4%. Any more shocks from climate related risks or geopolitical crisis will keep the outlook on domestic inflation tilted on upside. We expect inflation to average around 4.8% y/y in FY27 with risks tilted on the upside.

Domestic Liquidity -

- System liquidity, after moderating in the second half of March amidst tax outflows, improved in April as pressure from tax outflows waned and government spending picked up.

- RBI conducted a 4-day VRR auction for Rs1 tn. The overnight rates remain comfortable towards the lower end of the LAF corridor.

- We expect durable liquidity to ease around Rs3.5-3.75 tn, with the government cash balances back to surplus of around Rs1 tn as of April 30, 2026.

Fixed Income Outlook –

- The Indian fixed Income market last month experienced significant volatility across segment primarily shaped by a major geopolitical conflict in West Asia, which spiked crude oil having its ramifications on INR as well as global yields. In midst of this global turmoil and uncertainty, RBI announced its monetary policy guiding the market on its rate, inflation and growth projections.

- The major driver for most of the parameters was the movement in brent prices which moved in the range of $95 to $118 on news of settlement and disagreements between US and Iran. The rise in prices also increased speculation about increase in local energy prices and its indirect impact, especially post poll in couple of states.

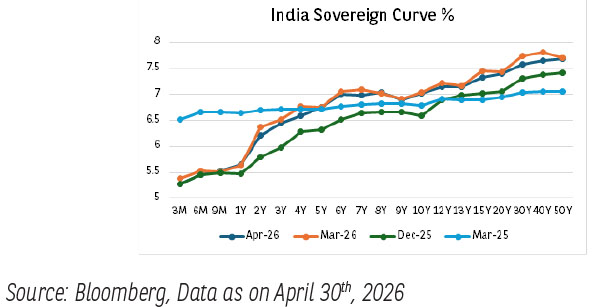

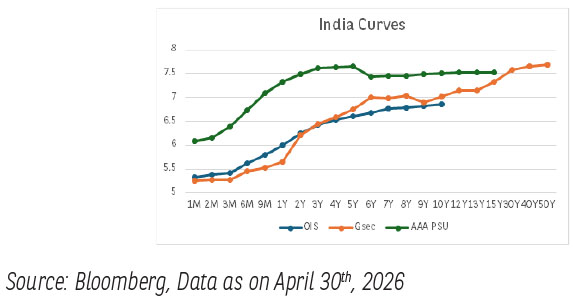

- The 10-year G-sec benchmark yields which ended in March 26 around 7.03%, up from almost below 6.75% levels in Feb 26 continued to face pressure in April 26. The 10-year benchmark G-sec yield witnessed volatility of 10-15 bps during the month making a high around 7.05% levels basis brent price behavior in addition to other factors like rising US yields around 4.40% levels and domestic concern on demand supply of Gsec and SDLs. Heavy supply pressure and absence of foreign demand for Indian debt during the month are expected to keep yields from falling sharply in the near term.

- Corporate bonds and SDL witnessed similar trends during the month as Gsec curve in light of continued supply and muted demand in light of the above factors. The spread for long Gsec ( esp. above 25 years) contraction of spread following reduced supply in light of the fact that the 10-year benchmark continued its upward journey during the month. Corporate bonds mainly in the 1-to-3-years maturity bucket were seen in demand as most of the fund managers preferred such bonds due to attractive accruals and lesser duration impact in a rising yield scenario.

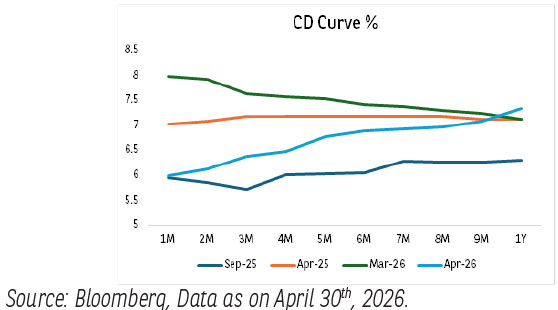

- At the shorter end, the curve witnessed some easing in levels up to 6 months following the March end phenomena and due to liquidity coming back to the banking system. As we moved towards one-year segment we witnessed overall stiffness in the levels above 7% following supply and other factors impacting overall yield curve.

- The RBI's Monetary Policy Committee (MPC) maintained the Repo Rate at 5.25% in its April 2026 meeting, keeping a "neutral" stance. The MPC remained vigilant, prioritizing data-driven decisions as supply-side shocks from the West Asia conflict introduce uncertainty. Headline inflation remains within the 2-6% target band, though projections for FY27 were recently raised to 4.6% due to energy and weather risks. GDP growth was projected at a robust 6.9% for FY27, slightly tempered from previous estimates due to global uncertainties. Despite domestic inflation remaining moderate (ticking up to 3.4%), the RBI maintained a neutral stance with a repo rate of 5.25%. High oil prices and global uncertainty have kept the RBI on a "long pause".

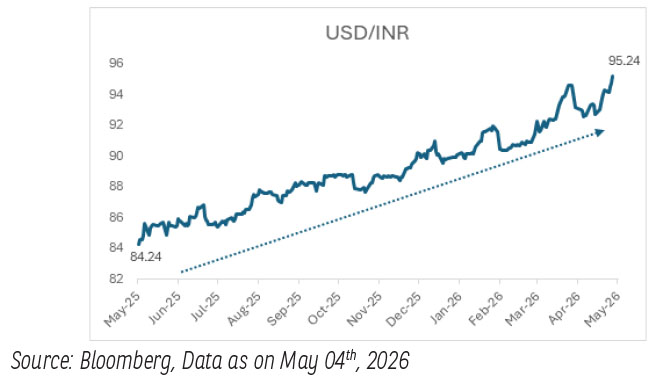

- The Indian Rupee (INR) underwent extreme volatility in April 2026, driven by geopolitical shocks in West Asia and persistent global dollar strength. The currency hit a historic low of Rs 95.33 per US Dollar, marking a steep 12% decline over a 12-month period. The Indian Rupee faced severe depreciation pressure, crossing the Rs 93–95 per dollar mark, which further incentivized the RBI to stay vigilant on liquidity and forex interventions.

Outlook:

- Going ahead, while structural tailwinds like global index inclusion persist, the market faces immediate pressure from a record borrowing calendar and geopolitical volatility. We recommend a barbell approach recommending core allocations in short-maturity bonds and money market instruments from accrual and spread perspective, while tactically positioning in long gilts and SDLs for any alpha generating opportunities.

The material contained herein has been obtained from publicly available information, believed to be reliable, but Baroda BNP Paribas Asset Management India Private Limited (BBNPPAMIPL) makes no representation that it is accurate or complete. This information is meant for general reading purposes only and is not meant to serve as a professional guide for the readers. This information is not intended to be an offer to see or a solicitation for the purchase or sale of any financial product or instrument. Past Performance may or may not be sustained in future and is not a guarantee of future returns.

Disclaimers for Market Outlook - Equity: The views and investment tips expressed by experts are their own and are meant for informational purposes only and should not be

construed as investment advice. Investors should check with their financial advisors before taking any investment decisions.

The material contained herein has been obtained from publicly available information, internally developed data and other sources believed to be reliable, but Baroda BNP

Paribas Asset Management India Private Limited (BBNPP), makes no representation that it is accurate or complete. BBNPP has no obligation to tell the recipient when opinions

or information given herein change. It has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. This information is

meant for general reading purposes only and is not meant to serve as a professional guide for the readers. Except for the historical information contained herein, statements in

this publication, which contain words or phrases such as ‘will’, ‘would’, etc., and similar expressions or variations of such expressions may constitute forward-looking statements.

These forward-looking statements involve a number of risks, uncertainties and other factors that could cause actual results to differ materially from those suggested by the

forward-looking statements. BBNPP undertakes no obligation to update forward-looking statements to reflect events or circumstances after the date thereof. Words like believe/

belief are independent perception of the Fund Manager and do not construe as opinion or advice. This information is not intended to be an offer to see or a solicitation for the

purchase or sale of any financial product or instrument. The investment strategy stated above is for illustration purposes only and may or may not be suitable for all investors.