Market Outlook

Market Outlook

| February 2026 |

|

|

In February 2026, Nifty Midcap 150 Index was up by 1.7% and Nifty Small Cap 250 Index by 0.7%. Sector wise majority of the sectors were in green with BSE Consumer Durables up by 7%, followed by BSE Healthcare (+6.2%), BSE Capital Goods (+5.7%), BSE OIL (+5.3%), BSE Metals (+4.1%), BSE Consumer Discretionary (+2.3%), BSE Bank (+1.6%). AI disruption led to BSE IT index being down by 18.7%.

FPI in February 2026 were positive with net inflow at 17 months high at USD 2.3bn. This is despite heavy selling in IT stocks amid AI concerns. However, this does not seem like a trend reversal due to geo-political tension and concerns over AI disruption. With regards to certain emerging economies, South Korea witnessed massive selling in February 2026 to the tune of USD 13.7bn. Taiwan continued to see positive inflow in 2026 to the tune of USD 8bn, followed by Brazil (+USD 2.9bn), Thailand (+1.7bn).

The US Supreme Court on 20th February 2026, rejected President Trump’s global tariff which was implemented under the national economic emergency law called the International Emergency Economic Powers Act (IEEPA). However, Trump administration has imposed a temporary 10% global tariff on imports from all countries under Section 122 of the Trade Act of 1974 as a short-term measure which will be constrained for a period of 150 days, and the tariffs can be increased to 15%.

On 28th February 2026, US and Israel launched a joint attack on Iran killing its supreme leader Ali Hosseini Khamenei. This has resulted in a war crisis in the Middle East, as Iran has retaliated with attacks on UAE, Kuwait, Quatar, Bahrain, Jordan, Oman. The war has led to severe challenges for oil & gas trade through Strait of Hormuz which controls almost 20% of global oil and gas supply. Closure, if any, and its duration will have a significant bearing on Oil & Gas price in near-term.

Locally, India markets came under sharp pressure, especially the IT sector due to AI led disruption after AI firm Anthropic unveiled new automation tools. Weakness also continues in Indian market on account of the on-going Middle East war with fear of increase in oil and gas prices which may impact corporate earnings in the near-term.

On the economic front, Purchasing Managers’ Index (PMI) manufacturing index rose to 55.4 in January 2026 from 55 in December 2025, driven by increased new orders, output and employment. PMI services rose from 58 in December 2025 to 58.5 in January 2026 driven by steady influx of new orders, including increased international demand from South and Southeast Asia. Net GST collection in January was up 7.6% YoY to INR 1.71tn and for financial year 2026 (April to January) was up 6.8% to INR 15.96tn.

Corporate India concluded its Q3FY26 earnings, with Nifty-500 delivering strong double-digit earnings growth, the highest in eight quarters, supported by improved sectoral breadth and benefits of new GST flowing through select sectors despite continued geopolitical headwinds. Aggregate sales/EBITDA/adj. PAT of Nifty-500 companies grew 11%/12%/19% YoY.

While we remain cautiously optimistic on Indian market on back for favourable government policies and improvement in corporate earnings growth in coming quarters, in the near-term middle east conflict will keep markets under pressure.

Source: B&K/ 360One, Kotak Securities, Motilal Oswal Financial Services

Global Economy –

The current global macroeconomic backdrop is once again being shaped by intensifying geopolitical fault lines. With fresh escalations in tensions between the United States and Iran, markets are repricing geopolitical risk at a rapid pace. Commodity markets have been the first to react, with brent crude breaking out of its prolonged lull, reflecting fears of supply disruptions and broader regional instability. As energy prices rise, inflation expectations risk becoming unanchored again, complicating the policy path for central banks that were only beginning to contemplate normalization.

The world is once again navigating a fragile equilibrium were geopolitical shocks feed directly into macro variables. Trade routes are being attacked, disrupting supply chains. Peace, it seems, has become both rare and expensive. In such an environment, doing business, deploying capital, and sustaining growth require far greater resilience than before. Investor confidence is becoming more vulnerable.

Risk and volatility have climbed up meaningfully. Global bond yields and currency markets are riding the waves of uncertainty, with vulnerable emerging market currencies facing renewed pressure. For countries heavily dependent on crude imports, the spike in oil prices threatens to widen current account deficits, strain fiscal balances, and delay growth recovery. Higher input costs, tighter financial conditions, and policy uncertainty are together making capital allocation more cautious and cross-border trade more complex.

Domestic Economy-

India’s new GDP series with base year FY23 stated Q3 FY26 growth at 7.8% y/y vs 8.4% y/y in Q2 FY26. Growth was primarily driven by manufacturing (its strongest growth in eight quarters) and services (it’s strongest in seven quarters).

On the demand side, both private consumption and investment remained robust. This is the first full quarter reflecting the impact of GST. Nominal GDP grew 8.9% in Q3 FY26, indicating a low deflator. In addition to the revision in base year from FY12 to FY23 the methodology broadens data collection and double deflation for manufacturing sector.

Economic activity in India continued to be resilient in January-26 and Feb-26, underpinned by upbeat demand conditions in both urban and rural areas. High frequency indicators for both urban and rural areas depict pickup in economic activity in start of 2026 led by post GST momentum, wedding season and robust proceeds from kharif harvest. Indicators of energy consumption, digital payments, trade and logistics. E-way bills continued to exhibit double digit growth. Rural demand strengthened further with retail sales of two-wheelers and tractors witnessing a pick-up in growth. Retail passenger vehicle sales continued to expand in January 2026, albeit at a slower pace. The sales slowdown reflects normalisation of markets following a period of high demand triggered by GST rate rationalisation. Domestic air passenger traffic recovered after the slump in December caused by the disruption in flight schedules.

One key positive development is the interim trade deal with the US announced on February 7,2026, wherein the US has agreed to lower the tariff rate on India to 18% from 50% earlier. With this deal in place the labour-intensive sectors and export-oriented industries in India are expected to receive a major support.

Prior to the US- India trade deal, India has also concluded major FTAs with UK, New Zealand and European Union. The most significant of the deals is India-EU FTA, with a combined market estimated at ~USD 24 trillion. The EU’s average tariff rate on Indian goods will drop from 3.8% to 0.1%. This could boost India’s exports and imports from EU which have been stagnant of late. EU accounts for ~17% of India’s exports and India enjoys a trade surplus with EU. More importantly, there is a comprehensive agreement on mobility for movement of skilled and semi-skilled professionals.

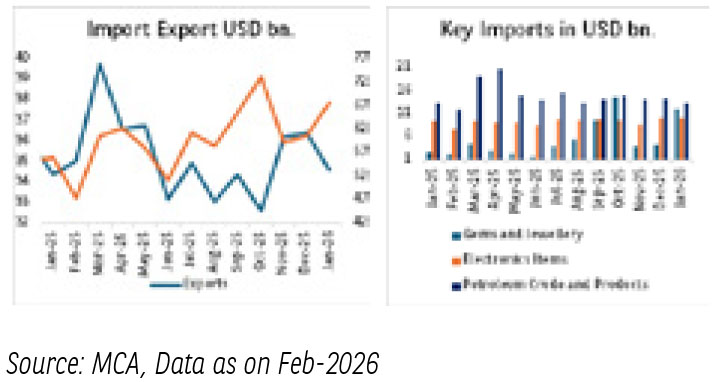

India’s trade deficit jumped to a three-month high in January-26 at US$34.7bn v/s US$25bn deficit in December -25. The rise in the deficit was led by gold imports which rose to US$12.1bn in January v/s US$4.1bn in December-25. Exports were lower by US$2bn MoM, led mainly by non-oil exports. India’s trade balances have faced headwinds from US tariffs to higher commodity prices. Another brewing headwind can arrive from pick up in brent prices as US Iran situation worsens. Therefore, INR mobility will largely depend on the core fundamentals of trade balances and thus can go sideways.

Domestic Inflation - New Series

- Headline CPI inflation in Jan-2026 stood at 2.75%, based on the new CPI series with the base year as 2024.

- The new base year series will reduce the volatility in headline inflation with lower weight to food inflation and higher weight to core inflation.

- The weight on core items in the new base year series has increased to 51% from 44.9% in old base year series. Meanwhile, the weight of food and beverages has declined to 40.1% from 45.9% in old base year series.

- In the new base year series, housing inflation is captured for both urban and rural areas compared to only urban areas in the old base year series.

- RBI assessment of underlying inflation momentum is unlikely to change with core inflation for previous months remaining in line with the new series.

- Given RBI’s projection for Q1 and Q2 FY27 inflation rising towards target levels and strong domestic demand conditions we expect RBI to remain on a prolonged pause.

Domestic Liquidity -

- RBI continued its liquidity easing measures, system liquidity conditions improved.

- Post that banking sector liquidity in India was at a surplus of Rs. 2.1 tn on February 26 compared to a surplus of Rs. 2.5 tn on February 18.

- The weighted average call rate (WACR) was at 5.08% on February 26 similar levels mid feb-2026.

- In Feb-2026, 1-Year median Marginal Cost of Funds based Lending Rate (MCLR) of SCBs increased to 8.45% in Feb-26 from 8.40% in Jan-26.

- We expect rates to remain closer to the lower end of the LAF corridor as system liquidity remains comfortable.

Fixed Income View -

Global Economy - The outlook remains uncertain with ongoing war. Higher brent prices are expected to seep in domestic trade numbers, pressuring current account deficit and further pressure on INR.

Overall transfer to domestic inflation remains limited as of now. But any prolong war like situation will pressure domestic economy through spillovers on trade, growth and inflation dynamics.

Domestic Rates & Policies -

- Post budget, till early feb-2026, we saw domestic bonds markets went in a sell off, with higher than anticipated gross borrowing number at Rs. 17.2 trn.

- Additionally higher SDL borrowing too dented the sentiments.

- This led to elevated rates and spreads.

- Recently, New CPI data along with much softer-than-expected core inflation aided the bond market sentiments.

- RBI policy maintained its pause on repo but the language on pre-emptive liquidity measures gave confidence on comfortable liquidity conditions going forward. Therefore, later we witnessed overnight rates to have fallen below repo.

- The bond market sentiments got another lift after the government announced a switch with the RBI, reducing the FY2027 maturities by Rs 75,000. The gross borrowing amount has accordingly reduced to Rs16.4 tn for FY27.

- We expect the current elevated spread in short to medium tenor corporate bond curve offers value in core allocation of the portfolio.

- Tactical allocation to high spread long tenor asset has the potential to generate alpha in the portfolio.

The material contained herein has been obtained from publicly available information, believed to be reliable, but Baroda BNP Paribas Asset Management India Private Limited (BBNPPAMIPL) makes no representation that it is accurate or complete. This information is meant for general reading purposes only and is not meant to serve as a professional guide for the readers. This information is not intended to be an offer to see or a solicitation for the purchase or sale of any financial product or instrument. Past Performance may or may not be sustained in future and is not a guarantee of future returns.

Disclaimers for Market Outlook - Equity: The views and investment tips expressed by experts are their own and are meant for informational purposes only and should not be

construed as investment advice. Investors should check with their financial advisors before taking any investment decisions.

The material contained herein has been obtained from publicly available information, internally developed data and other sources believed to be reliable, but Baroda BNP

Paribas Asset Management India Private Limited (BBNPP), makes no representation that it is accurate or complete. BBNPP has no obligation to tell the recipient when opinions

or information given herein change. It has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. This information is

meant for general reading purposes only and is not meant to serve as a professional guide for the readers. Except for the historical information contained herein, statements in

this publication, which contain words or phrases such as ‘will’, ‘would’, etc., and similar expressions or variations of such expressions may constitute forward-looking statements.

These forward-looking statements involve a number of risks, uncertainties and other factors that could cause actual results to differ materially from those suggested by the

forward-looking statements. BBNPP undertakes no obligation to update forward-looking statements to reflect events or circumstances after the date thereof. Words like believe/

belief are independent perception of the Fund Manager and do not construe as opinion or advice. This information is not intended to be an offer to see or a solicitation for the

purchase or sale of any financial product or instrument. The investment strategy stated above is for illustration purposes only and may or may not be suitable for all investors.