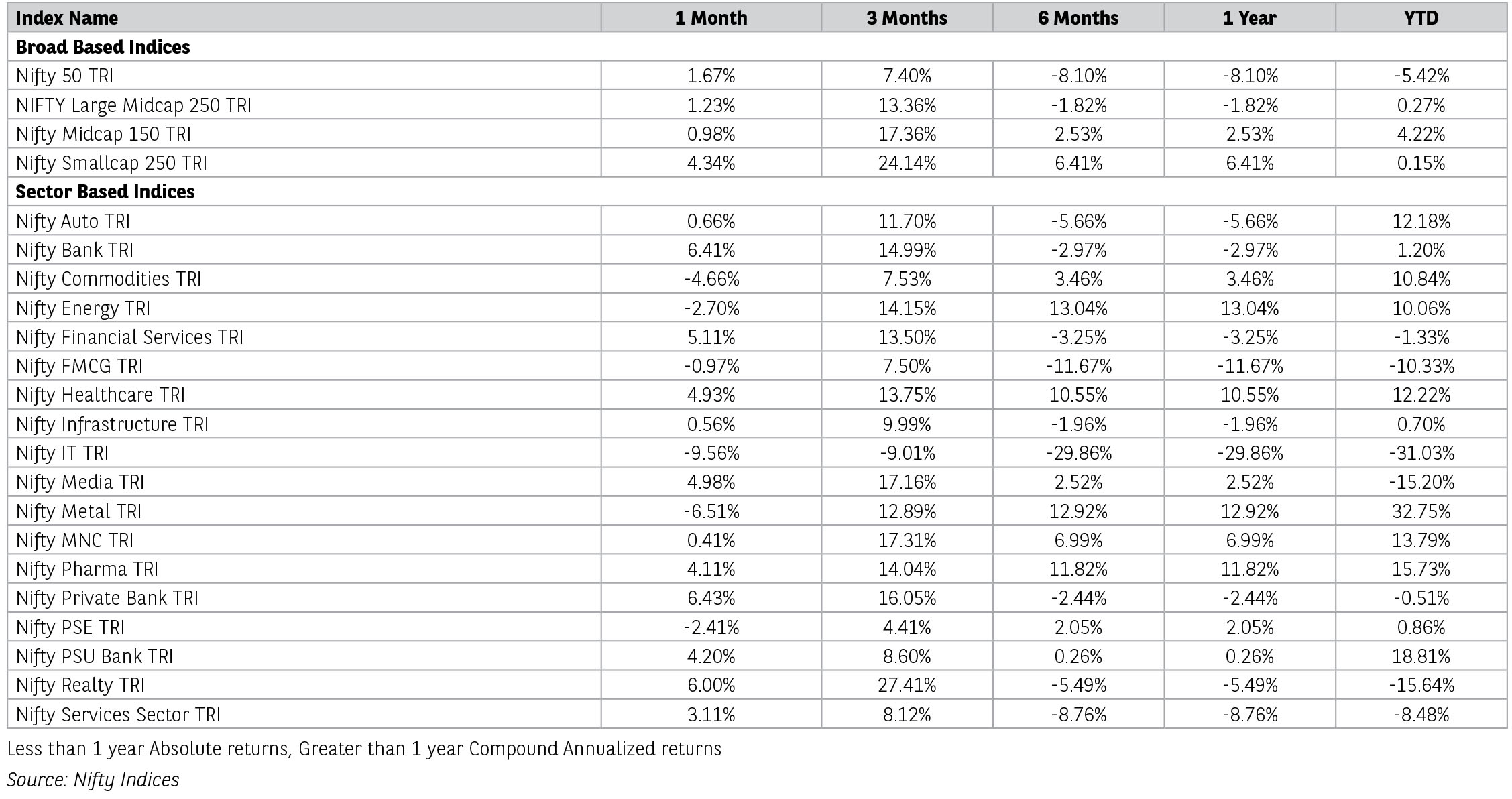

Market Outlook

Market Outlook

| June 2026 |

|

|

Amongst global markets, after a sharp rally in Asian markets led Artificial Intelligence (AI) theme, the month saw massive sell-off. Hong Kong’s Hang Seng Index was down by 9.1%, while South Korean market (KOSPI) was flat. Japan’s NIKKEI 225 Index rallied the most, up by 5.6%, followed by Taiwan Index (+3.1%) and Chinese index SSE Composite (Shanghai Stock Exchange) which was up by 0.6%.

Amongst developed European economies French CAC 40 Index was up by 2.7%, followed by FTSE 100 Index (UK) by 0.6%, while German index DAX was down by 0.7%. US index Dow Jones was up by 2.3% led by sector rotation to financials, healthcare and industrials, while S&P 500 was down by 1.8%, snapping its two month rally over concerns on Big Tech’s massive capital spending on AI.

Amongst mid and small cap index, small cap index outperformed the broader market, while mid cap although positive, slightly underperformed - Nifty Small Cap 250 Index was up by 4.3% and Nifty Midcap 150 Index was up by 0.9%. Within sectoral performance IT index continued to decline with BSE IT down by 8.7%, followed by BSE Metals and BSE Oil by 8.1% and 2.7% respectively on account of weakness in global commodity market and crash in crude oil prices. Amongst other sectors, BSE Banks saw the highest rally up by 6.4%, followed by BSE realty (+5.9%), BSE Healthcare (+5.3%), BSE Consumer discretionary (+3.9%), BSE Consumer Durables (+3.4%) and BSE Capital Goods (+0.7).

Foreign institutional investors extended their selling spree for the month of June with net selling of USD 5.2bn led by soaring US bond yields, preference for developed markets and expensive valuation of Indian markets. Amongst emerging economies, South Korea saw second consecutive month of intense selling (-USD 30.5bn). Taiwan too saw intense selling to the tune of USD 18.2bn in the month after 2 straight months of positive inflows. Brazil saw net outflow of USD 1.7bn, followed by Indonesia (-USD 1b) and Vietnam (-USD 566mn).

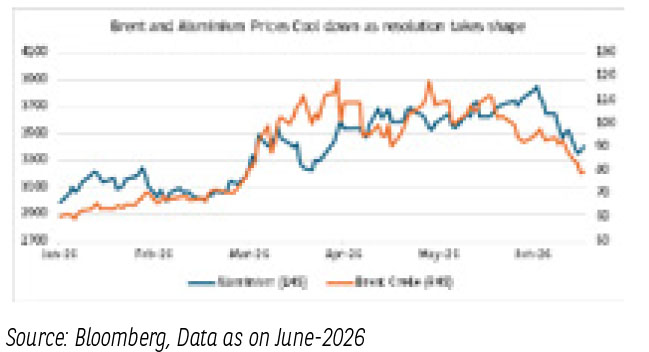

The West Asia war has come a temporary halt with both sides US and Iran agreeing to a 60-day ceasefire. Both the sides have signed a 14-point MoU for an immediate and permanent termination of military operations across all fronts. This has led to some respite in the global energy market, as with the opening of Strait of Hormuz crude oil prices have crashed by 40-45% from its peak. Although the concerns over the war has receded, global inflationary concerns persist which has led to global central banks adopt a more cautionary stance.

In the US, the Fed conducted its meeting under the recently appointed Chairman Kevin Warsh keeping the interest rates unchanged at 3.5-3.75% amid heightened inflationary pressure. The Fed Funds Rate forecast for 2026 rose to 3.8% from 3.4% in March, indicating one rate hike in 2026.

Locally, government of India has taken several steps to support depreciating rupee and policy changes to attract foreign investment participation in bond market. The Reserve Bank of India (RBI) has introduced a special forex swap window that allows banks to offer much higher interest rates up to 6-7.1% on 3-to-5-year Foreign Currency Non-Resident [FCNR(B)] deposits. The scheme is projected to attract USD 30-70bn in foreign currency and likely to support the falling rupee. Government has also recently announced an ordinance that removes the long-term capital gains tax to FII’s on their holdings in government securities. In this regard, government will eliminate the 12.5% long-term capital gains tax and the 20% withholding tax on interest income for eligible FIIs investing in Indian Government Securities. The RBI in its recent meeting kept the rates unchanged at 5.25% with a neutral stance.

Manufacturing activities inched up in May to 55 from 54.7 in April. Services PMI rose to 59.8 in May 2026 from 58.8 in April 2026. India’s retail inflation rose up to 3.93% in May 2026 from 3.48% in April 2026, driven by increase in food inflation and higher fuel prices. The Indian Meteorological Department (IMD) has forecasted monthly average rainfall in July to be below normal (less than 94% of LPA). In June 2026 the rainfall was 60% of Long Period Average (LPA). The strengthening of El Nino conditions and below normal rainfall will impact the kharif season. This can eventually lead to more pressure on inflation.

The concerns over inflation and profitability in 1HFY27 on account of West Asia war has reduced due to the ceasefire. While this supports the case for double digit growth in FY27, progress of monsoon will be key monitorable. Trailing Nifty valuations have now reverted to lower than the historical average to a PE of 18.8x as compared to its long-term average of 21x.

Source: Kotak Securities/Capital 360 ONE, Motilal Oswal Securities, Industry reports. Data as on June 30, 2026.

Global Economy –

The recent peace agreement between the United States and Iran has brought a much-needed sense of relief to global financial markets after weeks of heightened geopolitical uncertainty. The de-escalation of tensions has significantly reduced concerns over disruptions to global energy supplies, resulting in the gradual restoration of key supply chains and shipping routes across the region. Consequently, crude oil prices witnessed a meaningful correction from their elevated levels as fears of supply shortages subsided. The easing in energy prices also extended to other commodities, providing broad-based relief across global commodity markets.

Inflation expectations, which had risen sharply amid concerns over prolonged geopolitical conflict and supply-side disruptions, have begun to stabilise, offering policymakers greater confidence that price pressures may not intensify in the near term.

The implications for global bond markets have been immediate. Sovereign The decline in commodity prices has provided the global economy with a temporary reprieve from the volatile macroeconomic environment that had dominated financial markets in recent months.

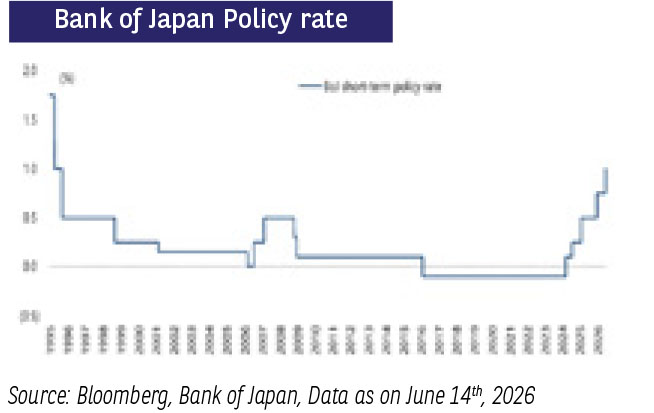

In June, major central banks adopted a cautious monetary policy stance amidst challenging growth inflation trade-offs. Amongst major AEs, while the Euro area and Japan pivoted to rate hikes in response to inflationary pressures, the US, the UK, along with other systemically important central banks held rates unchanged. Fed too kept the federal funds rate unchanged at the 3.5%–3.75% target range in June 2026.

Post the interim deal, Global bond markets reflected shift in sentiment, with sovereign bond yields retreating from recent highs as inflation concerns moderated and safe-haven demand eased. The correction in bond yields indicates that markets have become relatively more optimistic about the inflation outlook, reducing the immediate pressure on central banks to maintain an aggressively hawkish stance.

For monetary authorities across advanced and emerging economies alike, the moderation in inflationary expectations has offered a welcome breather after months of balancing the competing objectives of containing inflation while preserving economic growth. The immediate risk of renewed inflation driven by energy prices has diminished, allowing central banks greater flexibility in assessing incoming macroeconomic data before taking further policy actions.

Despite these encouraging developments, it would be premature to conclude that the global economy has moved beyond its recent challenges. The peace agreement marks an important step towards restoring stability, but the broader macroeconomic landscape continues to remain fragile and susceptible to fresh shocks. Geopolitical risks have not disappeared entirely, global trade continues to face structural challenges, and uncertainty surrounding economic growth persists across several regions. Elevated public debt levels, uneven recoveries across economies, lingering trade tensions and evolving monetary policy trajectories continue to pose downside risks to the global outlook.

Domestic Economy-

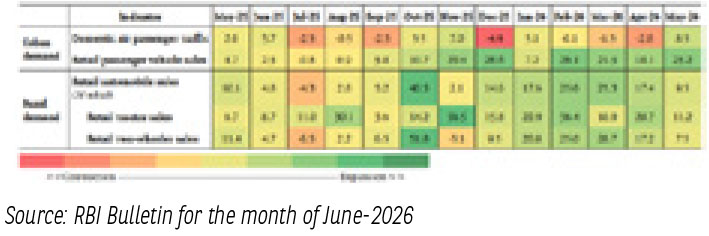

Domestic high frequency indicators reflect buoyant economic activity. Industrial activity remained robust and the services sector showed resilience, supported by pick-up in urban demand. Year on year growth in the domestic air passenger traffic recouped in May-2026 after contracting for three consecutive months. Growth in passenger vehicle sales accelerated with new product launches and healthy booking. India’s gross GST revenue stood at INR1.95t in Jun-2026 (INR1.71t in Jun-2025 and INR1.94t in May-2026), registering a 13.9% YoY growth vs a growth of 3.2% in May-2026. The growth was mainly driven by a sharp rise in GST from imports (34.6% YoY in Jun-2026).

Monsoon continues to be an area for concern for the Indian economy, especially rural. The progress of the South-West monsoon has been delayed with the formation of El Nino conditions. Till June 23rd, the cumulative rainfall deficit is tracking at 42% (below Long Period Average). The last time such a high level of June deficit was seen was in FY15. The cumulative rainfall deficit (June to September) during FY15 was 12%. Despite the extremely weak start, area under sowing shows a moderate pickup compared to last year, tracking higher by 1.7% YoY, as of June 19th, 2026. Crop-wise detail indicates that the rise is led by rice, coarse cereals, and pulses. Around 11% of total kharif snowing has been completed till June 19th, similar to last year. Another positive is that reservoir levels remain on the higher side at 113% of the 10-year average; however, they are below last year’s levels (87% of last year), as of June 18th, 2026. Record buffer stocks of rice and wheat are likely to provide cushion against any adverse impact of El Niño.

Domestic Inflation-

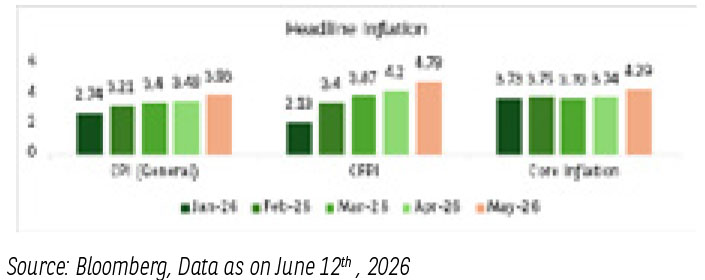

- CPI inflation rose to 3.93% y/y on May-2026, slightly higher than our expectations of 3.8% and lower than market expectations of inflation print to be above 4%. The headline number picked up sequentially by 0.75% m/m in May-2026, fastest pickup in last 10 months.

- Contribution wise headline number was driven by increase in petrol, diesel, gold, silver, airfare, vegetables, meat and poultry and rural fuel wood prices.

- The current resolution between US and Iran is expected to offset major upside risks to inflation.

- As the resolution comes into effect the volatility from West Asia crisis and its impact on energy prices and supply is expected to decline and thus the current crude prices fell below $72/bl.

- Risks to domestic inflation now remain from El Nino-related disruptions and heat waves.

- For the month of June-2026 we expect headline number to witness higher contribution from food inflation and slower momentum in pickup of core inflation as major shocks from West Asia war pressuring core, are now expected to recede.

- Also, on the monetary policy front, continued sub-4% inflation readings along with softening crude oil prices, if sustained, could provide RBI more room to be on a wait and watch mode in the August policy.

India fixed income markets outlook June 2026

During the month, fixed income, commodities and forex markets witnessed significant changes driven by aggressive and co-ordinated policy intervention by the Reserve Bank of India (RBI) and the government. RBI shifted the policy narrative towards inflation management as against growth and its announcements of various capital flow measures led to expectations of a massive surge in global capital inflows which fundamentally altered market dynamics during the month and going forward.

The RBI monetary policy committee (MPC) held its policy repo rate unchanged at 5.25% at its June 5th meeting, which was a unanimous decision in line with broad market expectations. The MPC revised its FY27 CPI inflation projection upward to 5.1% (from 4.6%), citing energy shocks from the West Asia conflict and El Nino-related food price risks, while trimming its FY27 GDP growth forecast to 6.6% from 6.9%.

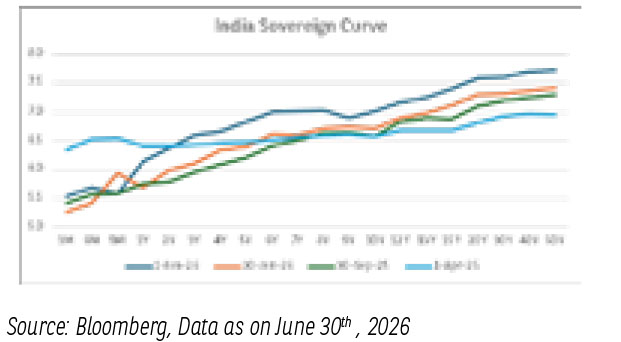

The Indian bond market rallied sharply, with 10-year Gsec yield falling to around 6.75% levels. Yields declined materially across the curve through June, with the move most pronounced at the long end. The 10-year benchmark opened the month at 7.02% and closed at 6.75%, a rally of ~25 bps. The 30-year fell from 7.65% to 7.27%, while the 2-year compressed from 6.37% to 5.96% The bullish sentiment was driven by cooling crude prices following de-escalation of middle east tension and strong foreign portfolio inflows and liquidity supportive measures from the RBI in addition to statement by RBI Governor Sanjay Malhotra stating it was "premature" to discuss rate hikes, pushing back against market expectations for tightening.

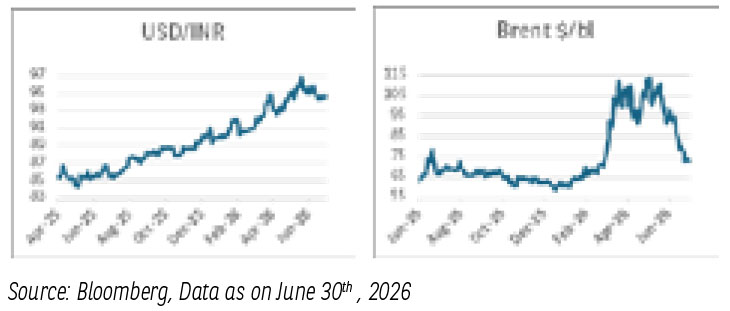

The Indian Rupee (INR) faced severe global crosscurrents in early June, touching historic lows near 96.60 per dollar in late May/early June. This prompted defensive currency optimization measures from the central bank;

- The government issued an emergency Income-tax Ordinance scrapping all capital gains and interest income taxes on G-Secs for global institutional investors

- The RBI added all new 15, 30, and 40 year government securities into the Fully Accessible Route (FAR) category, maximizing index-inclusion appeal

- This led to vibrant inflows from foreign portfolio investors through Fully Accessible Route (FAR) into sovereign segment

- Brent crude collapsed and stabilized near $70 per barrel following a West Asia de-escalation, significantly tempering near-term inflation anxiety.

- The RBI announced it would bear the entire foreign exchange hedging cost until September 30, 2026, for banks raising fresh 3 to 5 year Foreign Currency Non-Resident deposits.

- State-owned enterprises (PSUs) were granted special dollar swap windows to incentivize External Commercial Borrowings (ECB).

- The legal timeframe for realizing export proceeds was aggressively shortened back to nine months from 15 months to force quicker dollar repatriation into local banks.

These announcements led to positive expectations from dollar inflows perspective and cooling crude prices along with sustained FPI inflows ultimately lead to appreciation in INR from almost INR 96/- per dollar to close to INR 94.50/- per dollar during the month.

June 2026 marked a meaningful inflection for the corporate bond market. The tax exemption for foreign investors, the RBI's dovish tone, and improving geopolitical conditions drove record FAR inflows, a rally in G-sec yields, and a recovery in corporate bond activity after a weak start to FY27. Corporate spreads remain somewhat elevated relative to April levels, but the yield trajectory turned decisively lower through the month.

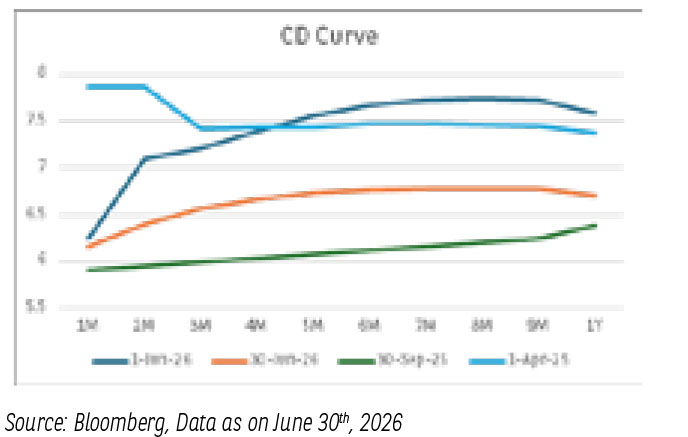

Following the announcements and changing market conditions markets almost recovered from the May 26 rise in yields across segment with 1Y to 10Y segment falling almost by 60-80 bps during the months.

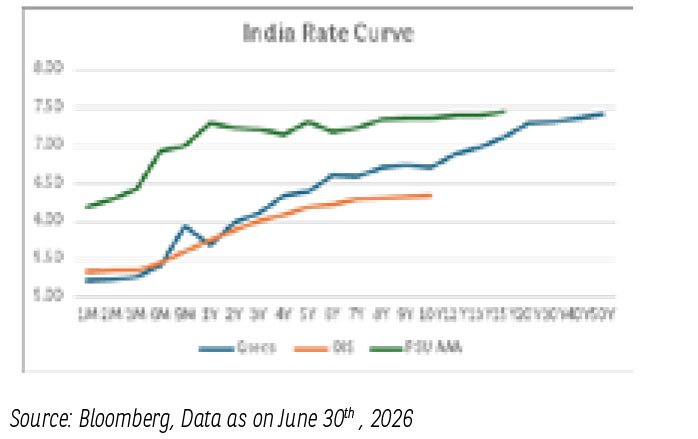

Liquidity was hovering around INR 1.50 lakhs in the beginning of the month which gradually declined post advance tax outflow, but the market action was contrary to changing liquidity scenario due to expectations of better liquidity conditions post announcement of RBI measures in the policy. Money market levels reflected the changing market dynamics with yields upto 12 months falling by approximately 50-70 bps.

The near-term backdrop for Indian fixed income is constructive, supported by dovish RBI signalling, record foreign inflows, and easing geopolitical tensions. However, the rally in G-secs from ~7% to 6.75% has been swift, and the risk-reward at current levels is more balanced. The short-to-medium part of the curve (2–5 years) offers the most attractive carry relative to risk. Corporate bonds stand to benefit from spread compression on expectations of liquidity comfort going ahead and postponement of rate hikes towards end of FY 27.

The material contained herein has been obtained from publicly available information, believed to be reliable, but Baroda BNP Paribas Asset Management India Private Limited (BBNPPAMIPL) makes no representation that it is accurate or complete. This information is meant for general reading purposes only and is not meant to serve as a professional guide for the readers. This information is not intended to be an offer to see or a solicitation for the purchase or sale of any financial product or instrument. Past Performance may or may not be sustained in future and is not a guarantee of future returns.

Disclaimers for Market Outlook - Equity: The views and investment tips expressed by experts are their own and are meant for informational purposes only and should not be

construed as investment advice. Investors should check with their financial advisors before taking any investment decisions.

The material contained herein has been obtained from publicly available information, internally developed data and other sources believed to be reliable, but Baroda BNP

Paribas Asset Management India Private Limited (BBNPP), makes no representation that it is accurate or complete. BBNPP has no obligation to tell the recipient when opinions

or information given herein change. It has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. This information is

meant for general reading purposes only and is not meant to serve as a professional guide for the readers. Except for the historical information contained herein, statements in

this publication, which contain words or phrases such as ‘will’, ‘would’, etc., and similar expressions or variations of such expressions may constitute forward-looking statements.

These forward-looking statements involve a number of risks, uncertainties and other factors that could cause actual results to differ materially from those suggested by the

forward-looking statements. BBNPP undertakes no obligation to update forward-looking statements to reflect events or circumstances after the date thereof. Words like believe/

belief are independent perception of the Fund Manager and do not construe as opinion or advice. This information is not intended to be an offer to see or a solicitation for the

purchase or sale of any financial product or instrument. The investment strategy stated above is for illustration purposes only and may or may not be suitable for all investors.