Market Outlook

Market Outlook

| May 2026 |

|

|

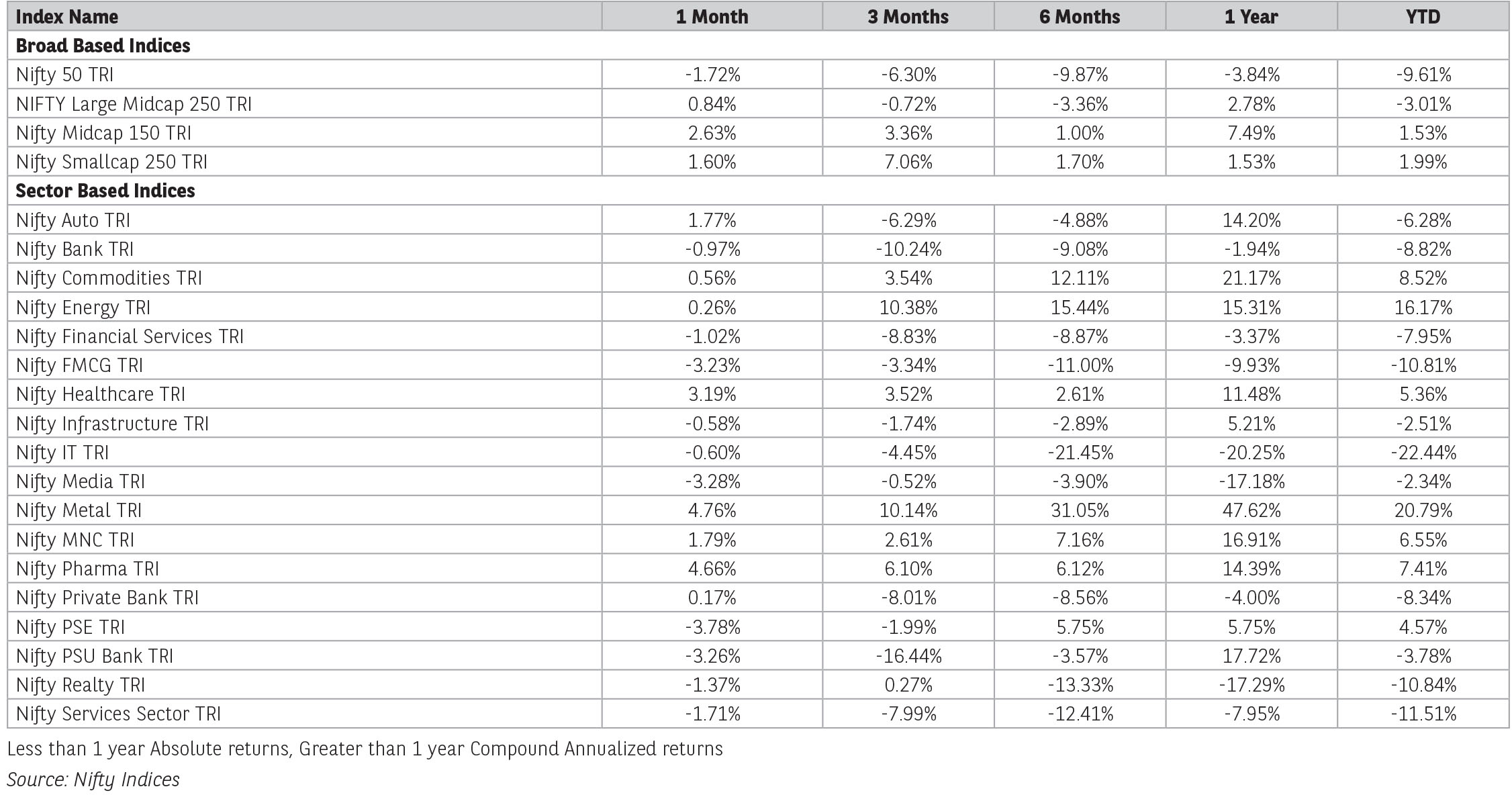

Amongst global markets, Asian indices again outperformed with South Korean market (KOSPI), Taiwan Index, Japan’s NIKKEI 225 Index up by 28.4%, 14.9% and 11.9% respectively. Apart from Artificial Intelligence (AI) and Semi-conductor theme, companies saw strong growth in earning driven by chip super cycle. which supported the market. Chinese Index SSE Composite (Shanghai Stock Exchange) was down by 1.1% and Hang Seng Index by 2.3%.

Amongst developed European economies German index DAX was up by 3.3% followed by French CAC 40 Index (+1.2%) and FTSE 100 Index (UK) by 0.6%. US index Nasdaq was up by 8.4%, while S&P 500 was up by 5.1%.

While the broader market was negative for the month of May, mid and small cap index outperformed led by healthy quarterly numbers. Nifty Midcap 150 Index was up by 2.6%, while Nifty Small Cap 250 Index was up by 1.6%. Sectoral performance was a mixed bag as sectors such as BSE Oil, BSE Consumer Durables, BSE IT, BSE Banks were down by 3.4%, 2.4% and 0.9% respectively. BSE Healthcare was up by 4.9% followed by BSE Cap Goods (+4.7%), BSE Metals (+3.7%) and BSE Consumer Discretionary (+0.3%).

Foreign institutional activity remained intense during the month with net selling of INR 559.6bn on account of global macro headwinds, weakening rupee and rising crude oil prices. Amongst emerging economies, Brazil after four months of positive flows, saw net outflow of USD 2.8bn. South Korea saw the highest sell-off to the tune of USD 27.9bn, followed by Vietnam (-USD 721mn). Taiwan saw the highest inflow of USD 8.3bn followed by USD 110mn in Thailand.

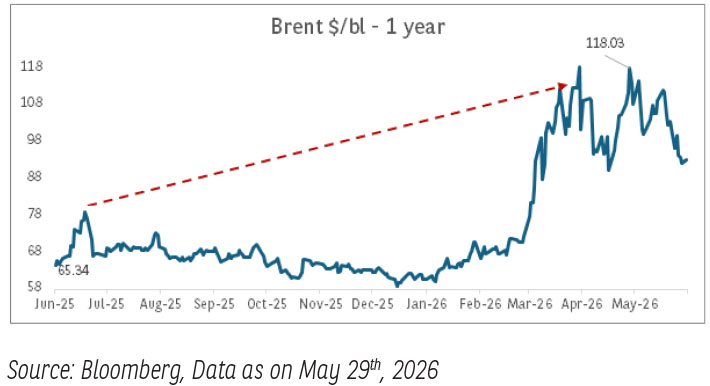

With regards to the on-going West Asia Crisis, the US and Iran have not yet come to a neutral ground on peace talks, and The Strait of Hormuz continues to remain closed. This has also disrupted the crude oil prices which has remained near the USD 100/barrel. With high energy prices, global financial conditions have tightened amid increasing inflationary risk. Most of the Central Banks have turned cautious on the policy outlook as bond yields rise globally and expectation of rate cuts have come down. Last month IMF cut its global growth forecast by 20 bps and highlighted that in an adverse scenario growth can slow down to 2-2.5%.

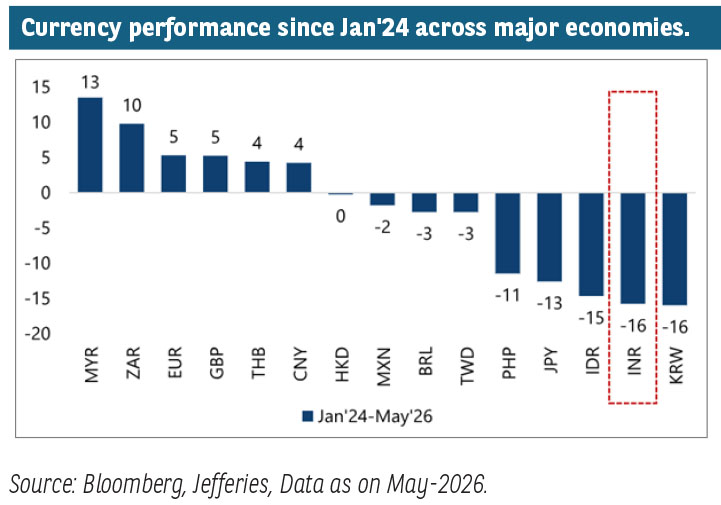

Locally, corporate India concluded its Q4FY26 quarterly numbers with NSE500 companies reporting Sales/EBITDA/PAT growth of 13%/12%/16% respectively. Although Q4FY26 earnings were healthy, a key monitorable will be the impact of the West Asia crisis for the upcoming quarters. Due to the current global headwinds, India’s Balance of Payment (BoP) and Current Account Deficient (CAD) are key monitorable. Indian Rupee continues to weaken against US$.

Manufacturing activities inched up in April to 54.7 from 53.9 in March. Services PMI rose to a five-month high to 58.8 in April from 57.5 in March. India’s retail inflation inched up to 3.48% in April, rising for the fourth consecutive month. With the imminent onset of monsoon season in India, the India Meteorological Department (IMD) has predicted overall rainfall in India to be ~90% of the long period average, due to the possibility of the El Nino effect. This has historically given rise to a scenario of food inflation and slowdown in rural demand. While the initial current reservoir levels appear to be adequate, this may mitigate some of the extreme impacts of the monsoon deficiency.

While the current season was strong and more so for the mid and small cap companies, the impact of high crude oil prices, disruption in supply chain and elevated logistics prices is yet to be seen on profitability. With the expectation of double-digit growth in FY27, resolution of the West Asia conflict, progress of monsoon, will be key monitorable. Trailing Nifty valuations have now reverted to lower than the historical average to a PE of 20.3x as of May-end, as compared to the 10-year average trailing Nifty PE of ~23x.

Source: Kotak Securities/Capital 360 ONE, Motilal Oswal Securities, Industry reports. Data as on May 31, 2026.

The ongoing West Asia crisis has once again brought geopolitical risks to the forefront of global markets, with uncertainty becoming the defining feature of the current macroeconomic landscape. At this juncture, perhaps the biggest challenge for policymakers, investors and businesses alike is the lack of clarity on how the crisis may evolve and the extent to which it could disrupt global trade, energy markets and capital flows. Consequently, volatility across asset classes ranging from equities and bonds to commodities and currencies has taken centre stage, reflecting heightened nervousness around inflation, growth and financial stability.

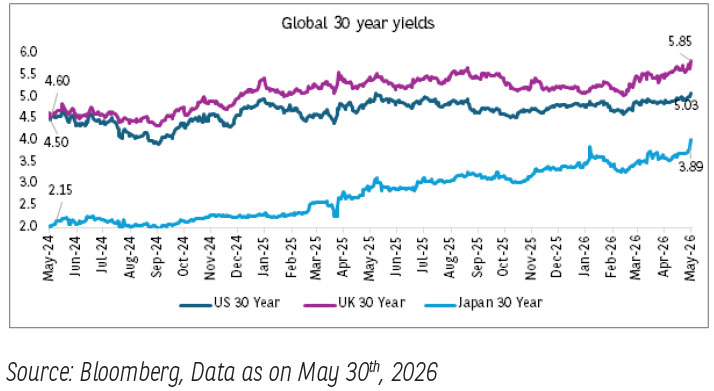

The implications for global bond markets have been immediate. Sovereign yields across major economies have picked up as investors reassess inflation expectations and recalibrate interest rate trajectories. Markets are increasingly pricing in the possibility that central banks may not have the room to pivot towards accommodative policies as quickly as previously anticipated. Instead, elevated energy and commodity prices risk keeping inflation sticky, compelling monetary authorities to maintain a cautious and relatively hawkish stance. In several economies, this could imply a longer pause in policy easing, while in others, the possibility of further rate hikes cannot be entirely ruled out should inflationary pressures intensify meaningfully.

This evolving macro backdrop presents a particularly difficult challenge for crude oil-importing economies, especially emerging markets that remain heavily dependent on external energy supplies. A sustained rise in crude prices has translated into significantly higher import bills, widening trade deficits and placing additional pressure on current account balances. At the same time, external headwinds are intensifying as tighter global financial conditions and elevated yields in advanced economies reduce the attractiveness of emerging market assets. Such dynamics are resulting in capital outflows and currency depreciation, further exacerbating imported inflation through costlier energy and commodity imports.

Domestic Economy-

The Indian economy demonstrated mixed signals amidst persisting geopolitical and trade related uncertainties. The available high-frequency indicators of economic activity in April reflected sustained demand but not broad based across sectors. Automobile sales in rural areas continued to grow at double digit in April, although showing some sequential moderation. The tractors and two-wheelers sales within automobile segment in rural and passenger vehicles sales in urban areas continued to witness robust growth. With an increase in prices of aviation turbine fuel, the air passenger traffic declined further. IIP grew 4.9% y/y in Apr-26 vs. 3.2% in Mar-2026 however on a sequential basis it contracted 9% vs. +9.5% MoM in March-2026 led by broad-based deceleration in growth across sectors barring mining, which grew at a faster pace. The merchandise trade deficit widened in April 2026 over March 2026 primarily on account of crude oil and gold imports. The surge in imports of precious metals prompted the Government to raise custom duties on gold, silver, and platinum.

Domestic Inflation-

- Headline CPI picked up marginally to 3.5% y/y in April-2026 from 3.4% in March-2026.

- Retail inflation was largely contained with moderate increase in food prices and limited pass through of higher fuel prices.

- Additionally precious metals like gold and silver declined in April-2026 vis a vis March-2026.

- We expect food prices to increase selectively and not broad based.

- With ongoing hikes in retail petrol and diesel prices we expect another pass through of ~75bps in domestic inflation.

- We expect FY27 CPI inflation to average around 5.2-5.4% y/y as our base case scenario of the expectation that the West Asia crisis persists no longer than H1 FY27.

- If war persists for longer than the base case, inflation is expected to remain above 6% level in H2 FY27.

Domestic Economy-

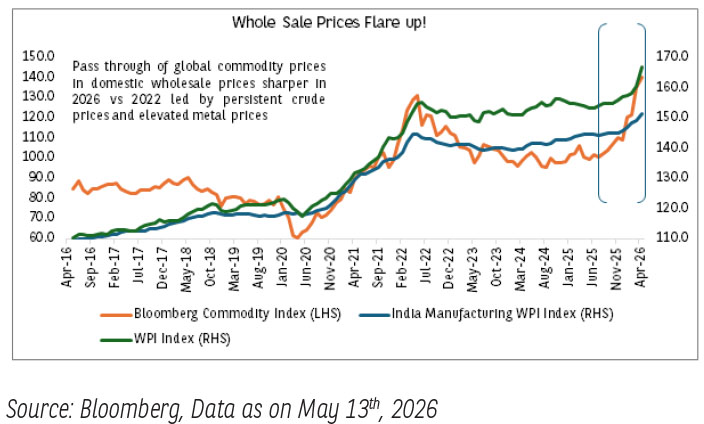

- Wholesale inflation flared up by 8.3% y/y in April-2026 highest in last 42 months, led by sharp & broad-based upturn in fuel prices and persistently elevated global metal prices.

- The direct linkages of global commodity prices to domestic wholesale prices have led to an immediate pass-through, and thus a sharp build-up of price pressures at the producer level.

India Fixed Income Review and Outlook:

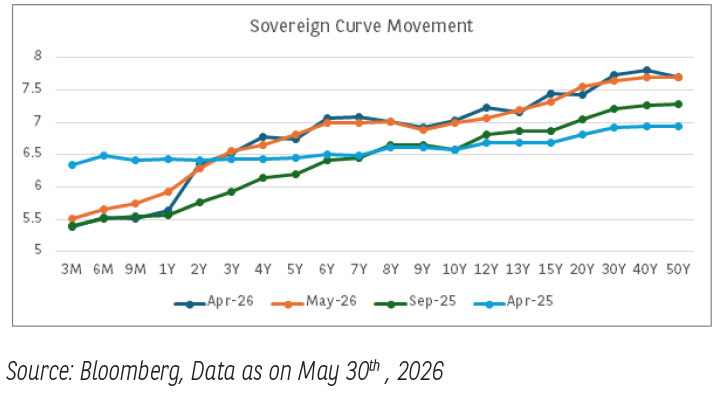

The Indian Fixed Income markets last month was mainly dictated by global geopolitical shocks which impacted surge in OIL prices past $100 per barrel range and proactive measures by the RBI to stem liquidity tightness. The crude oil spikes caused significant volatility across yield curves, RBI measures and dividend announcement imparted much required relief to strained liquidity last month.

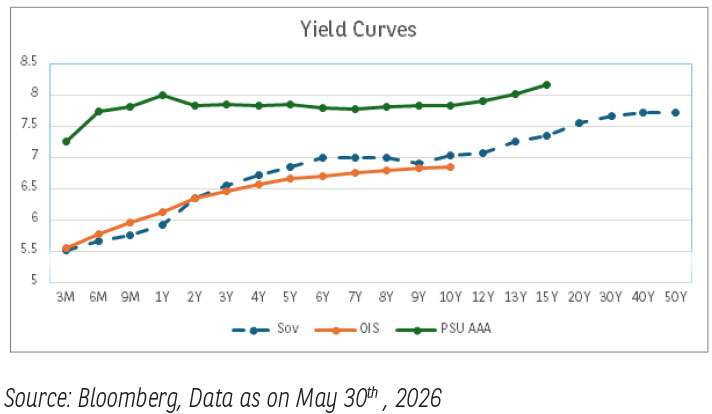

Overall, the markets witnessed volatility in yields to the tune of 20-25 bps during the month with 10-year Gsec benchmark making a low of almost 6.90% and a high of close to 7.10% before closing the month at around 7% due to factors like volatile oil prices, elevated US yields and liquidity supportive factors by the RBI. High quality corporate bonds and State Development Loans (SDLs) reflected Gsec yield movements with spreads hovering steadily around 50-65 bps across maturities. Though, we saw the shorter end bonds reacting to liquidity conditions throughout the month.

During the month, market participants began pricing in monetary tightening due to rising Oil prices and its impact on domestic prices going ahead, which led to expectations of rate hikes by the RBI later during FY 27. Yield spikes were capped later by structural optimism as finance ministry evaluated lowering withholding taxes on Gsecs to attract long term global index flows to boost Dollar inflow in the country. This move was probably intended to cushion the impact of higher US yields and boost India bond market allocation in global indices.

System liquidity fluctuated considerably during the month with temporary tightness initially which was attempted to ease with strong central bank interventions and RBI dividend.

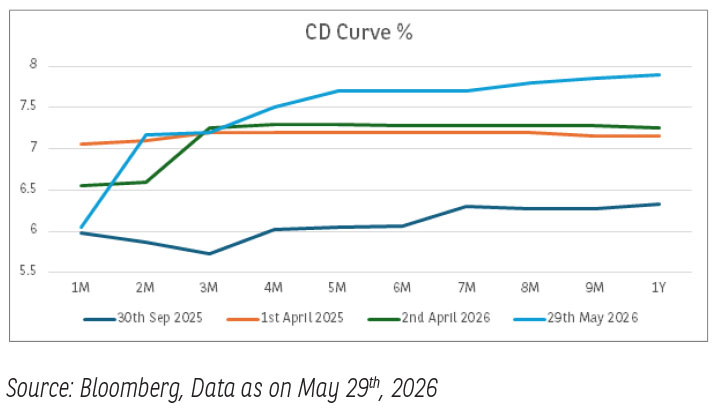

Banking system liquidity experienced a pronounced contraction during the month with surplus dipping briefly below INR 2 lakh crore as against last month’s surplus of almost INR 4 lakh crore. The deficit was driven mainly on account of intense FX stabilization measures to defend rupee against excessive volatility in addition to regular periodic outflows like GOI auctions and monthly GST outflows.

This led to excessive borrowing by banks, especially in CD market resulting in an increase in shorter end rates to recent highs across the CD/CP curve. The CD rates in 3 months to 12 months made a high of 7.50% to 7.90% before falling back by almost 20-25 bps on measures announced by the RBI.

RBI during the month resorted to multiple measures to stem liquidity problems. RBI announced multiple variable rate repo auctions ( VRR) in a bid to inject very short term liquidity to the market, in addition to the above RBI also conducted a $5 billion USD/INR Buy/Sell swap auction in which RBI bought USD from commercial banks to infuse durable long term rupee liquidity into the system, thereby easing some pressure on liquidity. RBI, also transferred annual dividend surplus to the government of around INR 3 trillion, which structurally anchored the short end of the curve.

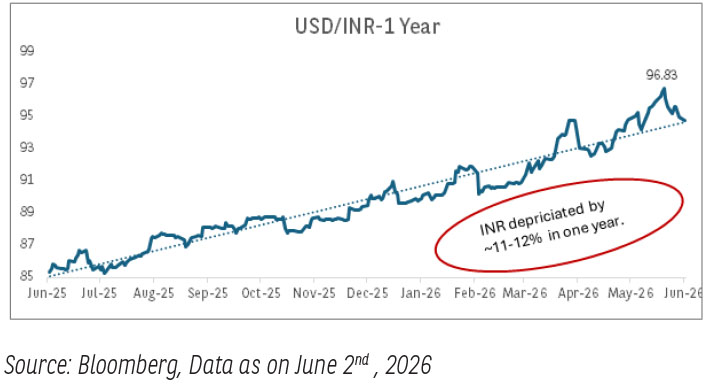

INR faced sustained pressure during the month against USD, driven by broad based global dollar strength and substantial foreign fund outflow following Indias situation in the ongoing global geopolitical crisis and elevated US yields scenario. The rupee faced steady pressures due to high global crude prices, month end dollar demand from domestic importers and a general risk-off sentiment. High US yields and expected corporate earnings growth in India relative to broader emerging markets prompted fund to relocate capital away from domestic markets. In light of the mounting pressure on the currency RBI announced measures to arrest the decline in the currency further.

Going ahead, market participants will watch the incoming data like monetary policy decisions, tax outflows, inflation, monsoons progress and GDP to position accordingly. In the current scenario an accrual-based approach, favoring high quality corporate bonds and structures, towards portfolio managements seems to be much more relevant. Duration can be a tactical approach for short term to generate alpha within the portfolios.

Source: RBI, Bloomberg, BBNPP Internal Research

The material contained herein has been obtained from publicly available information, believed to be reliable, but Baroda BNP Paribas Asset Management India Private Limited (BBNPPAMIPL) makes no representation that it is accurate or complete. This information is meant for general reading purposes only and is not meant to serve as a professional guide for the readers. This information is not intended to be an offer to see or a solicitation for the purchase or sale of any financial product or instrument. Past Performance may or may not be sustained in future and is not a guarantee of future returns.

Disclaimers for Market Outlook - Equity: The views and investment tips expressed by experts are their own and are meant for informational purposes only and should not be

construed as investment advice. Investors should check with their financial advisors before taking any investment decisions.

The material contained herein has been obtained from publicly available information, internally developed data and other sources believed to be reliable, but Baroda BNP

Paribas Asset Management India Private Limited (BBNPP), makes no representation that it is accurate or complete. BBNPP has no obligation to tell the recipient when opinions

or information given herein change. It has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. This information is

meant for general reading purposes only and is not meant to serve as a professional guide for the readers. Except for the historical information contained herein, statements in

this publication, which contain words or phrases such as ‘will’, ‘would’, etc., and similar expressions or variations of such expressions may constitute forward-looking statements.

These forward-looking statements involve a number of risks, uncertainties and other factors that could cause actual results to differ materially from those suggested by the

forward-looking statements. BBNPP undertakes no obligation to update forward-looking statements to reflect events or circumstances after the date thereof. Words like believe/

belief are independent perception of the Fund Manager and do not construe as opinion or advice. This information is not intended to be an offer to see or a solicitation for the

purchase or sale of any financial product or instrument. The investment strategy stated above is for illustration purposes only and may or may not be suitable for all investors.